Parsec Weekly #111

Hyperliquid - trouble in paradise?

Hyperliquid - trouble in paradise?

Never a quiet day in crypto! During a relatively quiet week where crypto prices at large were trending upwards, Hyperliquid has found itself in the spotlight once again.

Less than 2 weeks after HLP suffered a $4m loss, it has become the target of another highly profitable trading strategy (Avi Eisenberg reference for the uninitiated). Here’s a brief breakdown of what happened:

Trader opens massive $6m JELLYJELLY (obscure, low market cap coin) short on Hyperliquid

Trader begins to slam spot JELLYJELLY moving the oracle price higher

Trader pumps spot high enough to self liquidate their own short position

HLP as the backstop liquidator, inherits this oversized short position

As JELLYJELLY moves higher, HLP losses on the short position move higher, driving vault withdrawals

As users withdraw from HLP, positions are closed proportionally, to close JELLYJELLY short contracts HLP must buy them back into an empty-ish book, driving price higher and losses higher too

The unrealized loss at one point showed in excess of $13m. To put a stop to the bleed, Hyperliquid stepped in to delist JELLYJELLY perps, forcibly settling positions at a significantly lower price than the mark price on Hyperliquid and therefore erasing the loss HLP had on paper.

Despite the swift reaction, naturally this decision has caused quite some controversy. Some voicing concerns that this intervention lifts the veil of what has been a “decentralization theatre”. Gracy Chen, CEO of Bitget, even went as far as comparing the event to "FTX 2.0", which seems a little uncalled for.

The truth is that events like these act as a stark reminder than maintaining decentralization while preventing manipulation is simply very very hard and remains an unsolved problem.

I found @Galois_Capital’s commentary interesting, noting that this decision indicates that validators will choose to protect HLP at the expense of speculators which could create moral hazard, potentially leading to over-investment in HLP. Depositors know they can capture full upside but get bailed out in the event of big downside.

This shifts risk disproportionately onto MMs outside of HLP which could limit competition on Hyperliquid from a market making perspective. He is of the view that this ends up being good for HLP but bad for Hyperliquid (exchange and L1) in the long run.

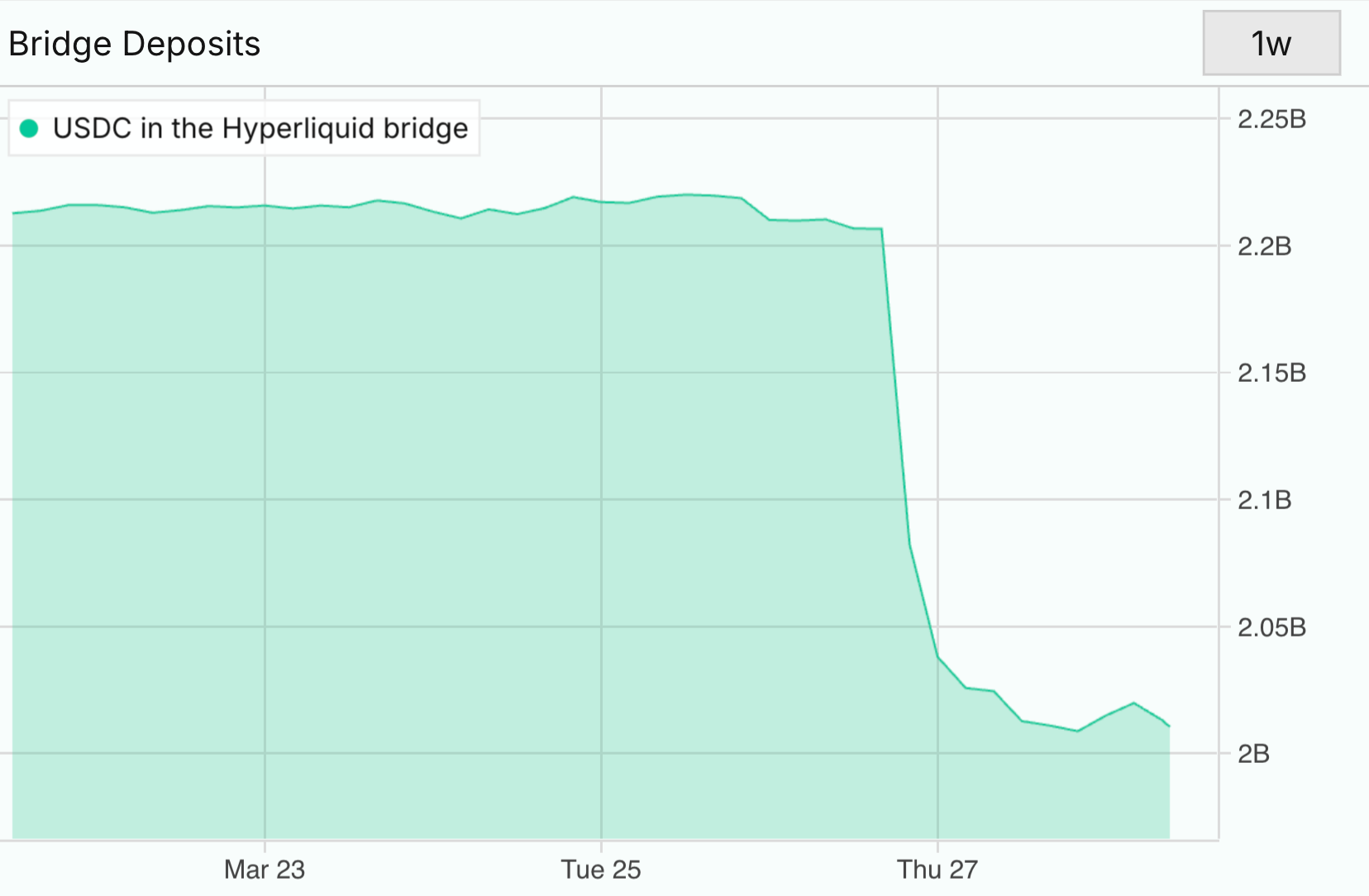

Despite the “re-imbursement” of HLP losses, bridge withdrawals from Hyperliquid have been significant and are not showing signs of reversing in the near term:

It's exciting