Parsec Weekly #95

The Return of the Basis Trade

The Return of the Basis Trade

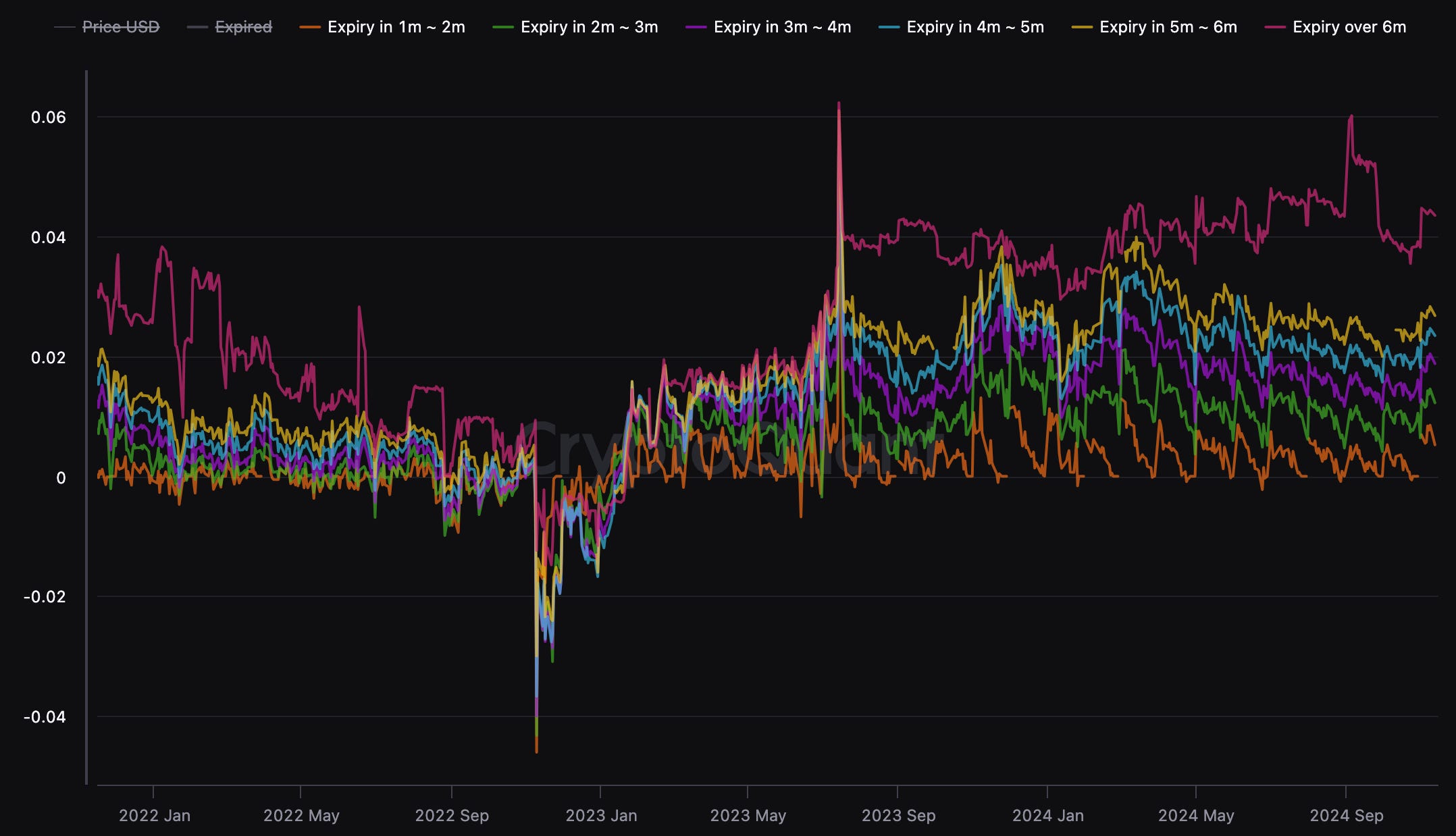

With BTC trading cleanly through $90k and animal spirits returning to the crypto markets, there’s plenty of activity afoot. While perhaps for Crypto natives, it feels as though the rampant speculation is only concentrated in memecoins, CEX and CME funding rates point to a significant increase in leverage on the majors.

Despite claims that significant tradfi flows have come to service this demand for leverage via a <long IBIT short CME futures against> structure, basis is still nearing 20% annualised on many CME tenors and on average across the Crypto-native perpetual products.

This is having some 2nd order effects onchain and is presenting particularly strong tailwinds for Ethena with the sUSDe yield approaching 30%!

Naturally, this is producing demand for USDe, along with their other growth initiatives (USDe as collateral integrations). It recently surpassed 3 billion in supply again:

Equally, we’ve seen the yield bearing sUSDe flip sDAI+sUSDS (rebranded sDAI) in terms of supply. The risk free rate on chain doesn’t sound so interesting when you can generate 10%+ yields on stables almost anywhere you look!

A demand for leverage onchain has been visibly present through increases in rates for both USDC and USDT across spot lending markets too:

Just today it was announced that Ethena’s sUSDe will be enabled as collateral on Aave which will likely drive rates on stablecoins even higher as yield farmers begin to implement looping strategies to harvest the spread.

The return of high onchain rates is also presenting opportunities for yield traders on Pendle who have been somewhat starved of opportunities since the EigenLayer points farming catalyst played out over summer. For example, PT buyers are able to currently lock in a 20% fixed annualised yield on the sUSDe March expiry PT:

Whether you’re a bull or a delta neutral yield maximisooor, there’s plenty of money to be made in these conditions. Not a great deal on the table for bears though, it must be said!